Market Size

Residential mortgages generally fall into one of two categories: Agency — eligible for programs offered by Fannie Mae, Freddie Mac, or Ginnie Mae (FHA/VA) — and non-Agency. As of Q1 2017, Agency loans are approximately 85% of new originations. According to the Federal Reserve Board, mortgage debt outstanding in that year totaled approximately $10.3 trillion [1]. By contrast, the private (non-Agency) market consist of over $1 trillion of this balance. However, the importance of the non-Agency market is disproportionate to its market share, because non-Agency programs, typically sold through whole-loan execution, are often where lenders can find a niche to differentiate themselves from the competition.

First Lien Residential Originations per MBA [2]

2017 Estimated $1.627 T – 67% Purchase Money

2016 Estimated $1.891 T – 52% Purchase Money

2015 Estimated $1.679 T – 52% Purchase Money

Agency vs. Non-Agency Loans

Fannie Mae, Freddie Mac, and FHA/VA issue guidelines defining the loans that they will purchase. Banks, mortgage companies, and other originators, generate loans that meet those guidelines, allowing consumers access to multiple sources of home lending. Originators compete on rate, price, and service, while providing consistent access to standardized financing vehicles offered by the Agencies. This creates liquidity in the market by providing a known source of funding for mortgage lending.

The non-Agency market, comprising loans that are not purchased by the Agencies, serves a different tier of consumer, many of whom have been left out of the housing recovery due to the drastic reduction in capital for non-Agency mortgages since the market down-turn began in 2007. These customers may not qualify for an Agency loan for any number of reasons, including lack of credit history, self-employed income, inconsistent employment history, excluded property type, or loan balance. non-Agency loans are typically originated by banks to be held on their balance sheets. This risk is typically priced at an interest rate of 50-150 basis points (bps) over Agency paper.

Non-Agency Loans in the Secondary Market

In the mid-2010s, mortgage lenders began venturing into new products that are further down the credit curve and/or allowing for impairments that previously may have resulted in prohibitive risk-based pricing adjustments. Specifically, larger community banks were underwriting portfolio mortgages to higher loan-to-value ratios (LTVs), lower FICOs, and/or alternative doc types. Generally, only one of the three criteria deviated from what makes a loan Agency-eligible; another way to say this is that portfolio lenders seek to avoid excessive risk layering. Banks still need to be able to justify to regulators why they make a loan, and “the relationship” is not an acceptable answer. As this style of community-bank lending expands, the secondary market for these loans is currently outpacing origination. Other banks are willing to pay a premium for these loans, because they can avoid the overhead associated with retail loan origination, and the higher yields on the loans are adequate compensation for the (perceived or actual) incremental credit risk.

CRA

Mid 2017 has been a busy season for CRA transactions for MIAC. Historically, the CRA buying season does not pick up until the fall. In 2017 MIAC released a software tool that allows originators to parse their product by CRA credit eligibility. MIAC is uniquely suited to work with depositories to solve their CRA credit need. This investment in technology has allowed MIAC to more efficiently serve our Bank clients’ needs for Community Reinvestment Act credit.

Pricing for CRA loans has historically centered around 50-150 bps over TBA prices. Recent transactions have centered around 75bps over, which we feel reflects a discount to the true market price prior to demand increasing. This is due to the relatively fewer Buyers in the market, as well as efficiencies in transacting that MIAC has generated by relying on existing Agency clients to provide them an increase in price received while at the same time allowing Buyers to pay less than other Sellers are asking.

Non-QM Lending

The market has nearly doubled in 2017 from 2016 numbers, mainly because there are more lenders willing to expand their credit box. In 2016 there were relatively few lenders willing to lend to a challenged borrower at a reasonable rate. This allowed for a few major lenders to capture the majority of the market. In 2017, we are seeing more liquidity for these borrowers from banks, funds and increasingly, non-bank lenders. This has the dual effect of reducing rates through competition, which consequently increases demand for this product.

MIAC has transacted a substantial volume of these loans through our depository and fund clients. Using our robust suite of modeling and marketing tools we have been able to help Buyers understand the product and the Sellers to price the product correctly for a successful execution.

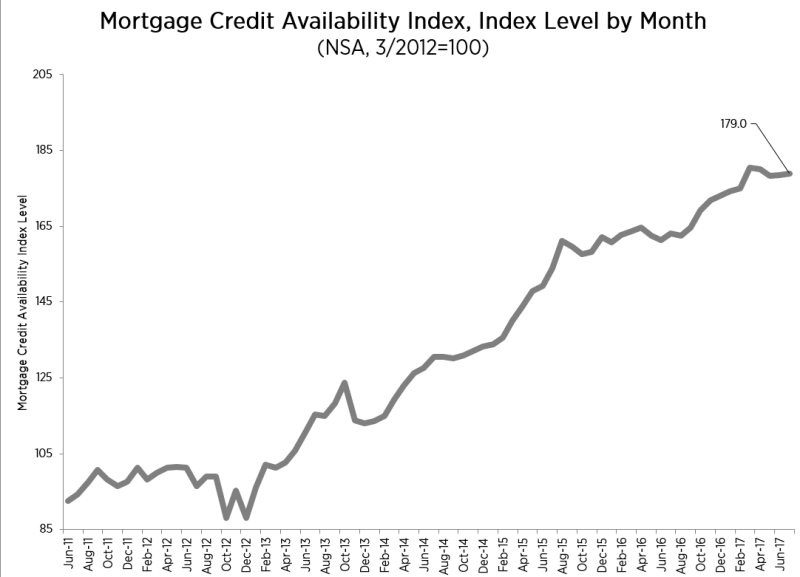

The growth we are seeing in Non-QM derives from both credit as well as collateral expansion. Borrowers with more severe credit defects as well are obtaining financing at higher LTVs than previously. Additionally, higher LTVs for strong borrowers who may not have income documentation or citizenship to qualify for Agency financing. See figure 1.

Figure 1: Source: MIAC Analytics

Pricing of Whole Loans in 2017

Non-Performing Loans

In early 2017 there was a 3-5% bump in pricing that Buyers were willing to pay for Non-Performing Whole Loans. With benchmark pricing centering around the upper 50s to low 60s through 2016, there were a number of larger transactions in the market that were well though this pricing. MIAC executed several trades in NPLs at the mid-60s+ level for Banks and Funds. NPLs are a very diverse market and it is difficult to draw direct correlations from one transaction to the next, however, it widely agreed that demand outstripped supply earlier this year.

More recently, there is increasing demand and supply, although robust, appears to broadly represent the “tails” of the market. There is currently a large ~$1b trade in the market from a bank that represents one the largest, non-government, transactions this year. When this clears the market, we will have additional color and would be glad to discuss.

Non-Agency

With the increased demand for yield by depositories, there is a greater money supply for borrowers outside of traditional Agency lending. MIAC sees this manifest in multiple ways; both an Increase in the number of lenders/banks that are willing originate a portfolio product as well as expansion of the credit box that is available. 90 LTV loans are much more common than last year when 80% was generally the ceiling and 65% in many cases.

Pricing has improved for the consumer, this is due to a number of reasons. In addition to the increase in willingness to lend, as there is a higher level of comfort with regulations in the Non-QM lending space. It was not too long ago that Non-Agency was nearly nonexistent, yet it is fairly common today with increased access to more consumers. Rates are typically 50-150 bps through Agency, with a greater spread as you move further from Agency guides. MIAC currently has two large transactions under contract with 3% yields for short-term paper.

Agency

Agency lending is very transparent and is broadly understood. Included in this pricing is the expansion of lending. Agencies are willing to purchase higher LTVs and lower credit scores than in 2016. There has been a push to increase home ownership, the easiest way to accomplish this is to lend to borrowers who previously were not credit worthy. The MIAC Agency desk Sells $3-4 billion of mortgages each month, providing significant insight into the market on a daily basis.

Execution of Whole Loan Sales

Buyers and Sellers of mortgage loans should insist on working with trading partners who are seasoned in transacting, performing valuation, and hedging as diverse a population of mortgage products as possible, with optimal results. This includes Agency-eligible pricing execution, seasoned mortgage performing, Prime Jumbo, Hybrids, RPL’s, NPL’s, HELOC, Reverse mortgage portfolio valuations, and hedging of a diverse population of mortgage products. It is important to work with a partner that sees as much trading and analytic activity as MIAC, which, by virtue of the breadth of its business activities, has frequent contact with most of the largest originators, funds, banks, and portfolio companies.

The most efficient traders must gather the current market intelligence needed to identify and engage the best execution for a given trade. There are timing considerations, external events that affect a buyer’s ability to focus on a trade, as well as other market considerations. This includes an intimate understanding of firms’ business models on both the buy and sell side, as well as their pricing requirements and investors’ “appetites.” Some dealmakers have, at best, a cursory level of understanding of investors’ objectives. The lack of depth of understanding often yields a sale that has been put out so widely (shown to too many unqualified buyers) that it becomes a trade that many serious funds will avoid.

Best execution comes from a complete understanding of the seller’s needs, both in terms of price and timing, and the credit and liquidity nuances of the portfolio. The dealmaker you work with must understand these nuances and match the trade with a proper number of serious buyers who will focus on the trade with a no-fade bid that will close with a very high degree of surety.

[1] https://www.federalreserve.gov/data/mortoutstand/current.htm

[2] http://www.mortgagedaily.com/ResidentialStatistics.asp

Brendan Teeley, Senior Vice President, Whole Loan Sales & Trading, MIAC Capital Markets

MIAC Perspectives – Fall 2017

Whole Loan Execution Update