Since last month’s issue, we added a “Research Insights” series to our Monthly Residential MSR Update. These Insights are designed to be both short and topical. Your feedback is essential to accomplishing these twin objectives. We welcome comments on existing articles as well as suggestions for future ones. The additional content will follow the MSR Market Update below.

Month-over-Month

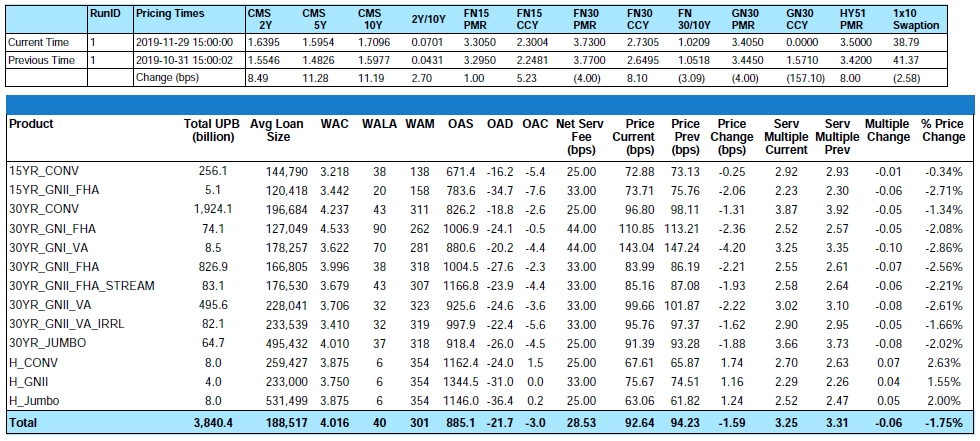

From end-of-month October to end-of-month November, the MIAC Generic Servicing Assets (GSAs™) Conv_30 Index decreased by 1.34%, and the GNII_FHA_30 Index decreased by 2.56%. In larger GSA cohorts, which are actively traded in the MSR market, the Conv30_3.5_2017 cohort decreased by 1.51%, and the GNII_FHA30_3.5_2017 cohort decreased by 2.70%.

During the month of November, Conv_30 Index OAS’s widened to close the month at 826.2 bps, for an increase of 7.6 bps. Likewise, GNII_FHA_30 Index OAS’s widened to 1,004.5 bps, for a month-over-month increase of 51.5 bps.

Figure 1: Month-over-Month Pricing Change by Product Source: MIAC Analytics™

From end-of-month October to end-of-month November, MIAC’s Primary Mortgage Rate decreased by four (4) bps to 3.73%. For a longer look back, from November 2018 to November 2019, MIAC’s Primary Mortgage Rate is now lower by ninety-five (95) bps. On a more positive note for MSRs, with Federal Reserve policy on cruise control and the economy continuing to grow at a steady pace, mortgage rates are showing some signs of stabilization. The risk of an economic downturn has given ground to a very strong job market and, going forward, what should be a slightly higher rate environment.

Looking ahead, consensus estimates currently point to a 10-year Treasury rate of 2.25% by the end of 2020, as diminishing tail risks from the trade war reinject term premium into the yield curve. Rising Treasury yields could bring 30-year mortgage rates up to 4.0% by 2020 year-end, which is above current levels, but still well below the peaks of 2018.

Figure 2: Conventional 30 Year Primary Mortgage Rate Source: MIAC Analytics™

While lower rates this year have been overall detrimental to MSR values, origination volumes seem to suggest that better years lie ahead. In combination with a housing market that is expected to remain strong in the near future even as the U.S. faces a likely economic downturn, Freddie Mac is now forecasting back-to-back years of $2 trillion in mortgage loan originations rather than the previously forecasted drop-off in 2020. While slightly at odds with the MBA forecast of $1.89 trillion for 2020 and Fannie Mae’s forecast of $1.86 trillion, it still represents an increase over prior period projections.

Figure 3: Year-to-Date Pricing Change by Product Source: MIAC Analytics™

Prepayment News

As expected, Conventional 30-year agency prepayments slowed in November to a 17% CPR vs. a 21% CPR in October. The slowdown was largely driven by seasonality and lower day count. In other prepay- related news, the share of Ginnie Mae MBS backed by VA loans reached an all-time high of 45% for recently issued pools. This is up from a 30% share for 2012 vintage Ginnie Mae pools. The VA concentration is especially high for lower coupon Ginnie cohorts, with 52% of Ginnie 3.0% pools being backed by VA loans vs. 22% for the Ginnie 4.5% pools. The trend is especially concerning for the Ginnie Mae sector given the high prepayment rates for VA loans. For example, within the 2018 vintage 3.5% coupons, VA loans prepaid at a 40% CPR in November vs. 24% for FHA loans, leading to substantially faster Ginnie Mae CPRs vs. Fannie Mae.

According to Black Knight, more than half of the 2019 3Q refinance activity was of the cash-out variety. After hitting an 18-year low in 2018 4Q, refinance volume has nearly doubled. Prompted by lower rates, the increase in people refinancing their mortgages was primarily to improve the rate and/or term, but cash-out refinances were also higher. During the third quarter of 2019, cash-outs made up 52% of all third-quarter refinances, with homeowners withdrawing more than $36 billion in equity, which is the highest amount withdrawn via cash-outs in nearly 12 years. To put this into context, it’s estimated that borrowers held about $6.2 trillion of tappable equity at the end of 2019 3Q which is up from $5.9 trillion one year earlier.

Recapture: To Include or Not?

Plain and simple: most large servicers now include, whether directly or indirectly, recapture as part of their GAAP value.

Firms with back-office call centers have virtually perfected the art of recapture, resulting in recapture percentages as high as 50% – 60%. Since the beginning of time, recapture has been a part of the discussion with the SEC, OCC, FASB and others. Auditors and regulators do not want to say no to the incorporation of recapture value into a GAAP compliant Fair Market Value in case liquid markets evolve to incorporating such a value, but they are skeptical about scoping in self-generated intangibles. If they trade and get compensated, which they do, it can have support in GAAP. If recaptured cash flows were not reflected in the MSR market pricing conventions of bidders, then auditors will challenge a firm that unilaterally elects to include recapture cash flows. However, the MSR market convention has evolved so that nearly every bidder on larger MSR packages will include recapture cash flows in the bid pricing methods. Given this widely accepted market convention, the inclusion of recapture cash flows in the MSR’s fair market value can be successfully defended to auditors.

MIAC’s MSR Valuation Committee believes that the market convention for bidders’ recapture rates are actually significantly lower than recently realized recapture rates. MIAC has product-specific market pricing recapture rates, however, none of these rates exceed 20% annualized recapture.

Other reasons why firms might exercise some caution:

1) The largest MSR holders have been using recapture in the recent MSR bids, however, they could elect to alter this behavior in the future.

2) A firm may discontinue paying up for recapture when/if bandwidth creates more volume than a firm is equipped to handle. Anyone believing that their ability to recapture may be compromised due to capacity constraints is not likely to include as much, or any, recapture benefit into their bid prices.

At MIAC, we model recapture as a prospective gain on sale and in a manner that is consistent with fair market trades or in the case of an economic value, the firm’s actual cash flow and valuation behavior. If you are contemplating direct or indirect inclusion of recapture into a fair market value, please feel free to reach out to your MIAC representative for further market insight.

MSR Transaction Activity

For anyone holding onto the belief that falling rates in 2019 crushed the amount of MSR transaction activity, think again. Through Q1 – Q3 of 2019, over $450 billion in Bulk- and Mergers and Acquisitions-related transfers have occurred. Factor in Co-Issue and that number rises to nearly $600 billion. As we approach the holidays, MSR transactions have slowed drastically (comparatively speaking) as very few servicers want to be in the office on the last business day of the year sending out wires. However, be prepared because with the New Year come new budgets, and early indications already point to an increase in January activity.

“Large” transactions, which we define as deals containing $1 – $5+ billion in unpaid principal balance, continue to validate our very granular GSA prices. As for smaller offerings, the price/multiple spread initially tightened, but depending on the trade and amount of buy-side interest is now showing some signs of widening. This is largely due to the previously referenced differences in the amount of recapture benefit being included into a buyer’s offering price. We have witnessed trades where the value attributed to recapture is zero bps, and others when the spread has been 12 bps (and a lot in between).

The smallest packages, categorized as $300 million or less in unpaid principal balance, are trading but at prices that “on average” range anywhere from 10 – 20 bps lower than the bid prices obtained on larger offerings. In addition to the increased economies of scale afforded by larger MSR trades, the acquisition cost is one of the reasons that smaller deals can trade at a discount to larger offerings. The legal and due diligence costs that a buyer typically incurs to acquire a portfolio, can influence how a firm might bid on a smaller trade. Even so, it is the smaller trades that can often create the largest margins. And in a quest for margin, increasingly we see larger buyers bidding on smaller offerings but usually with a more rigid approach to price and term negotiations.

Regardless of size, not all bids are as they might appear on the surface. Differences in prepay protection periods, non-reimbursable advances, non-payment for assets that are 60+ days delinquent, fee deductions for seriously delinquent MSRs, loan kicks, seller non-solicitation requirements, and possible set-up fees are just a few of the pitfalls that can quickly affect a seller’s net execution price.

Figure 4: Year-to-Date Conv 30-YR 3.50% 2019 GSA Index Source: MIAC Analytics™

MIAC’s MSR Valuation department provides MSR valuation advisory services to over 200 institutions totaling nearly $2 trillion in residential and commercial MSR valuations every month.

.

Residential MSR Market Update – November 2019

Author

Mike Carnes, Managing Director, MSR Valuations, Capital Markets Group

Mike.Carnes@miacanalytics.com

Research Insights: Liquidation Timelines – November 2019

This is the second edition of Research Insights, taking a closer look at liquidation timelines. Because this is a complex subject, this edition focuses on a few key themes. Additional details will be addressed in future editions of our Research Insights series.

What are Liquidation Timelines?

We define the liquidation timeline for a residential loan to be the number of months it takes to resolve a distressed asset, from initial delinquency through final resolution. In order to operationalize this concept, several conventions need to be adopted. For example, a loan may become seriously delinquent (hereafter, SDQ), cure back to current, become seriously delinquent a second time, and then finally resolve with a loss. This SDQ->Cure->SDQ cycle can occur repeatedly. The analyst needs to decide if the timeline should be measured from the first serious delinquency, the last, or some mixture of the two.

A second complication is that a loan can liquidate with a loss via many paths, such as completion of a foreclosure and REO sale, a borrower-titled short sale, or a third-party take-out. Short sales are very common in all residential sectors, so any measure of liquidation time needs to extend beyond just “time in foreclosure”.

We adopt a simple measure of liquidation timelines: Conditional on a loan liquidation, we record the number of months past due as of that liquidation date. This definition is both simple to apply to actual data, and fully consistent with our Core Residential Valuation Model. This realization-based measure (i.e., where we only sample fully resolved assets) avoids the censoring problems that can exist with other metrics.

Why Should Market Participants Care About Liquidation Timelines?

Liquidation timelines have a significant impact on loss severities. In turn, loss severities have a large impact on whole loan valuations, risk sensitivities (such as duration and WAL), and stress valuations. Loss severities are even important for loans with credit enhancement, such as private mortgage insurance or a VA guarantee, since there is usually some probability that the insurance or guarantee will not fully cover the actual loss. Liquidation timelines also play a vital role in an MSR context, for both valuations as well as advancing/cash flow analysis. The impact of liquidation timelines on MSRs will be addressed in a forthcoming Research Insights.

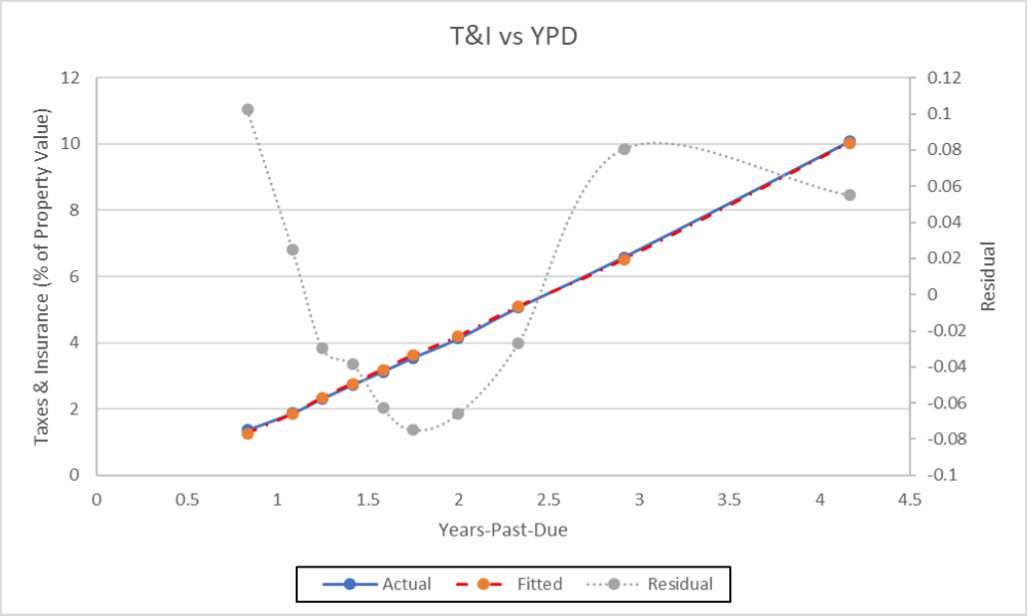

Figures 1-3 highlight the impact of timelines on various components of loss severity. Figure 1 shows the relationship between escrow (i.e., Tax and Insurance) expenses and the realized liquidation timeline. We represent timelines in terms of years past due rather than months past so that readers can interpret these data in annualized terms. The actual liquidation can be the sale of an REO property (where title is obtained via a completed foreclosure), the receipt of proceeds from a borrower-titled short sale, or any other foreclosure alternative.

Expenses are shown as a percentage of the estimated property value as of the dated date of the last paid installment. The underlying data is obtained from the FHLMC Loan Level Dataset. The predicted value of the Tax and Insurance loss component is obtained from the Core Residential Valuation Model. As is evident, escrow expenses increase linearly as a function of the realized liquidation timelines. States with higher average taxes or insurance costs will of course have a higher slope, and this is captured by our Model. A complete description of our Core Residential Valuation Model, which includes the Loss Severity sub-model, is available from your MIAC sales coverage.

Figure 2 is analogous to Figure 1, except that it displays maintenance expense (again, as a percentage of estimated property value) versus the realized liquidation timeline. The same pattern is evident, although there is a very mild quadratic effect at large values of years past due. Maintenance costs vary quite a bit across states, and this is also captured by our Model.

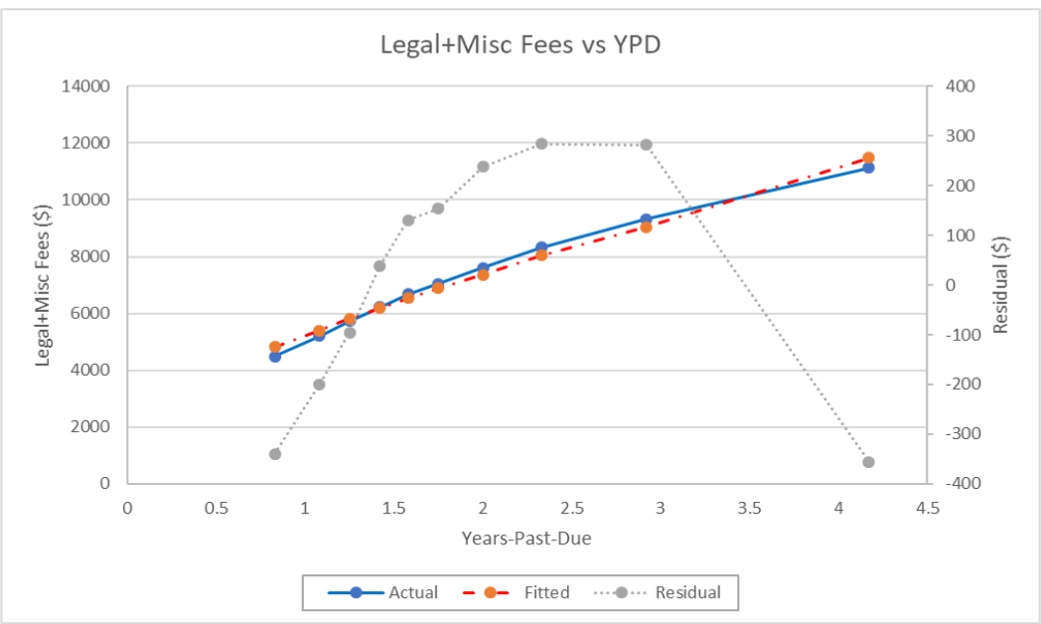

Finally, Figure 3 displays legal and miscellaneous costs (in $ terms, rather than as a % of estimated property value) versus realized timelines. Once again, we see the same pronounced effect of liquidation timeline on this important component of loss.

In contrast to the above three loss components relating to expenses, net proceeds from property liquidation (another significant driver of losses) has a very limited dependence on realized timelines after controlling for other variables such as mark-to-market LTV, UPB, occupancy and loan purpose.

It is well established that loss severities have increased substantially since the housing crisis. See, for example, the Federal Reserve Bank of Philadelphia Working Paper 17-08 entitled “Regime Shift and the Post-Crisis World of Mortgage Loss Severities”}. Figure 4 shows that this increase is due, in large part, to average liquidation timelines rising over this period, in fact, more than doubling between 2008 and 2016.

The Mechanics of Timelines in MIAC’s Core Residential Valuation Model

Our Core Residential Valuation Model was completely revamped in early 2019. This new model fully integrates the transition and loss severity sub-models. In order to explain what we mean by fully integrated some background is needed.

The responsibility of the transition model is to predict the probability that a given loan is in all feasible delinquency statuses at every month in the future. For example, consider a loan that starts out as current. The transition model will predict the probability that the loan remains current, transitions to D30, or prepays at the end of the month. At a horizon of 12 months, many more states are of course feasible, and our model computes the probability of all feasible states.

In any transition model, liquidation and prepayment are terminal (or absorbing) states. In other words, once a loan transitions to either loss liquidation or prepayment, it becomes and remains inactive. In contrast, serious delinquency (SDQ), foreclosure, and even REO are active states. For example, consider a loan that starts out as D120. That loan can cure to a less delinquent state, remain in serious delinquency, transitions to FCL, or liquidate via borrower-assisted short sale.

Within our model framework, we define the liquidation timeline as the expected months past due (equivalently, the cumulative number of missed payments) conditional on the loan having liquidated, at each projection month. Importantly, liquidation timelines are an outcome of our transition model framework. In other words, they are fully implied by our transition model specification, and no additional assumptions are needed.

To see this, consider a simplified framework where loans can only liquidate from a completed FCL and subsequent REO liquidation. In that case, the average liquidation timeline will be driven entirely by transition rate of SDQ to FCL (SDQ->FCL), the transition rate of FCL to REO (FCL->REO), and finally the transition rate of REO->LIQ. Any loan attribute or macro-factor which reduces those transitions will lengthen the average amount of time the loan spends in each state, and thus increase average liquidation timelines. In the more complex structure underlying the Core Residential Valuation Model, average liquidation timelines will also depend on the resolution mix predicted by the model, as we discuss below.

As indicated previously, the severity model and the transition frequency model are fully integrated. This means that the timelines predicted by the transition model are input into our loss severity model. In other words, the responsibility of the transition model is to produce expected timelines at every projection month, and the responsibility of the severity model is to consume those timelines and produce an expected loss.

The Evolution of Projected Liquidation Timelines in Core Residential Valuation Model

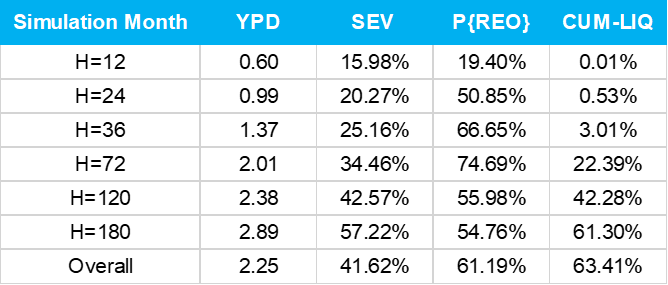

In order to highlight these ideas and explore some additional consequences of our Core Residential Valuation Model, we ran a hypothetical newly originated Agency loan with the following characteristics: $250k balance, 750 FICO, 75% LTV/CLTV. We decided to run a “synthetic average” Judicial state. By synthetic average, we mean that this is representative of Judicial states overall, and not of any single Judicial state in particular. We use this for our production runs on portfolios that are reasonably representative of Judicial states overall. As is well known, there is considerable heterogeneity within the Judicial/Power of Sale (POS) segmentation. It is perhaps less well known that there is segment overlap: the slowest POS states are slower than the fastest Judicial states. In a forthcoming Research Insights, we’ll delve into this topic in more detail.

The results of this analysis are displayed in Figure 5. The most significant observation is that expected timelines continuously increase over time (i.e., as the loan seasons). This is partly the result of the REO/Short-sale mix changing across projection months. Conditional on a loan liquidating early on, there is a higher probability that it was short sale resolution. However, timelines would also increase over time if short-sales did not exist and all liquidations were the result of foreclosure/REO resolutions.

Primarily because of the increase in expected timelines, expected severities will increase over time as well. Consequently, it would be highly imprudent to “guestimate” a deal’s long-term severity by looking at severities observed over the first few years. As the above discussion makes clear, those are likely to be the lower severities that the deal will ever experience.

Figure 1 Source: MIAC Analytics™

Figure 2 Source: MIAC Analytics™

Figure 3 Source: MIAC Analytics™

Figure 4 Source: MIAC Analytics™

Figure 5 Source: MIAC Analytics™

.

Research Insights: Liquidation Timelines – November 2019

Author

Dick Kazarian, Managing Director, Borrower Analytics Group

Dick.Kazarian@miacanalytics.com

Download the entire Monthly Update as a PDF