American Bankers Association President and CEO, Rob Nichols, in a news release called the new accounting standard “the biggest change in the history of bank accounting.” He added, “While we continue to have strong concerns with the costs related to CECL’s life of loan loss concept, we are committed to working with both regulators and auditors to ensure banks of all sizes can meet the implementation challenges of the new standard.”

Current Expected Credit Loss (CECL) represents a dramatic adjustment for banks, credit unions, and financial institutions, regardless of asset size. Recent accounting pronouncements differ from precedent as follows:

- Reserving thresholds will be raised, but the new pronouncements also allow institutions to apply judgment in developing estimation methods that are appropriate and practical for their circumstances

- New standards are forward-looking for both reserving and capital adequacy, based upon expectations of future cash flows under plausible scenarios, rather than on historic losses to date.

- Heightened data storage and analytical requirements will apply, and firms will need to coordinate between functional areas, in order to accurately focus judgment for the forecasting of expected losses

The revised standard effectively formalizes the forecasting of expected credit losses on loan assets. MIAC models expected credit losses for loan valuations using our proprietary system, MIAC Analytics™, and no firm prices more loan assets than MIAC.

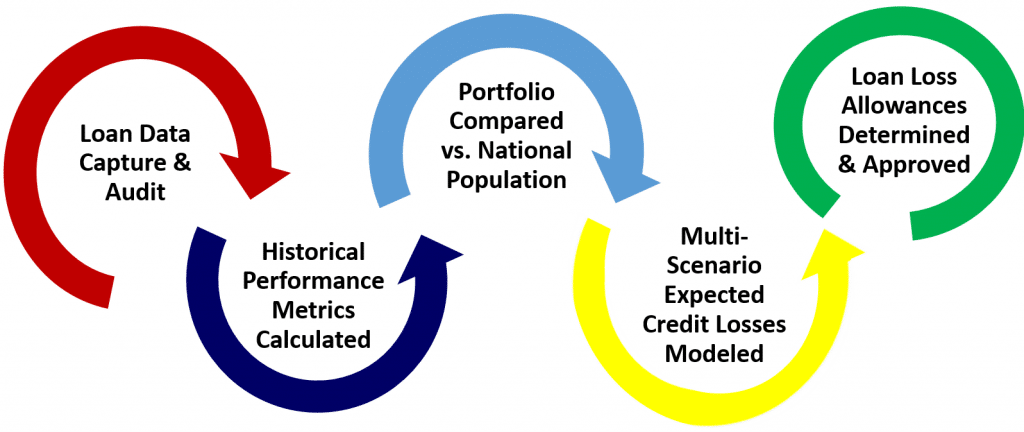

MIAC’s CECL Process is comprised of these elements…

Download MIAC’s Free CECL Process Guide

Our proprietary CECL tools were developed internally to execute these requirements:

- DR-Surveillance™ is used to marshal retrospective metrics on lender performance

- MIAC CORE™, our residential borrower behavior model, is tuned to forecast future results for determination of loss allowances, using institution-specific data

Below we describe these MIAC applications, their functionality, and inter-connectivity.

DR-Surveillance™ and MIAC CORE™

Measuring the key loan performance metrics, and then using them in forecasted cash flows is the key to CECL. But specific portfolio collateral behavior is only one part of the solution: comparing results against the collateral performance of a larger population of very similar loans is a much more meaningful and useful procedure. MIAC maintains historical loan performance of nearly 100 million loans that can be used as national reference benchmarks, to help firms determine the relative performance of their loan pools over time in DR-Surveillance™.

Utilizing our large dataset, MIAC can measure the asset specific, geographic specific, and institution specific behavioral response to the requisite macro factors – HPI, CPI, GDP, unemployment, and interest rates.

In addition, we have precisely measured borrower behavior while in foreclosure, including cure rates, REO entry rates, timing of REO entry, and timing for Cure from FCL.

Therefore, MIAC’s estimates of future credit loss, and forecasts emanating from our proprietary systems, are relied upon throughout our industry, the accounting profession, and across multiple government agencies.

CECL’s preliminary tenets were provided by FASB, with joint OCC, FDIC, NCUA and FRB guidance.

FASB News Release June 16th, 2016 – AUS Financial Instruments – Credit Losses (Topic 326)

Read MIAC’s Perspective: CECL – Current Expected Credit Loss: A CORE Competency?

Download MIAC’s FREE CECL Process Guide

CONTACT

CECL@miacanalytics.com