Overview of the Rules

CECL overhauls the current impairment models for loans, leases and debt securities, and also impacts commitments. It removes the “probable” threshold under the “incurred loss model” for recognizing credit losses.

Firms will be required to report the current estimate of lifetime loan losses, incorporated into the Allowance for Loan and Lease Losses (ALLL). While a discounted cash flow (DCF) approach was considered by FASB in exposure drafts, the final standard allows any approach, as long as it is reasonable. Institutions, Auditors and Regulators will decide, so early discussions are encouraged.

Both quantitative and qualitative methods are to be utilized jointly. Although there is a strong a bias to the use of cash flow models with assumptions powered by quantitative data with “reasonable” scenarios, a historical loss-based result which could meet the standards.

CECL requires that estimates for losses be based on relevant information about past events, including both qualitative and quantitative factors, such as historical loss experience with similar assets, and then-current conditions. Evaluations of the borrowers’ creditworthiness through reasonable, supportable forecasts that demonstrate the expected collectability of the remaining assets contractual cash flows is encouraged.

Predictive models are commonly based on historical experience/quantitative data. Reasonable forecasts and conditional assessments are qualitative in nature, as they provide a forecast and estimates

Other qualitative factors include changes in:

- Lending policies and procedures, collections, etc.

- Experience of management and staff

- Quality of the loan review system

Financial assets carried at amortized cost less a loss allowance reflect the current expected cash flows to be collected, and income statements will reflect credit deterioration or improvement.

For financial assets carried at fair value (FV) with fluctuations recognized through other comprehensive income (OCI), the balance sheet would reflect fair value, but the income statement would reflect credit deterioration or improvement.

Under some circumstances, institutions can elect not to recognize expected credit losses on assets held at fair value. The conditions are that the FV equals or exceeds the amortized cost and if expected credit losses are immaterial.

What Will it Take to Implement CECL?

An array of new processes will be required. Policies and procedures will need to be revamped in management, governance, risk reporting, controls and functional integration.

Program Management will be the start: newfound coordination among functional areas such as finance, originations, credit, operations and technology, and a revised governance and risk management framework.

Segmentation of loan, lease and debt portfolios into clearly identifiable portions with similar and discrete characteristics is the next step.

Importantly, dual jurisdiction reporting institutions – CECL and IFRS 9 – firms will need to:

- Handle 12 months (IFRS 9) versus lifetime (CECL) credit loss projections and reporting in models and report generation

- Estimate credit losses for future draws on commitments for IFRS and for commitments that cannot be unconditionally canceled for CECL

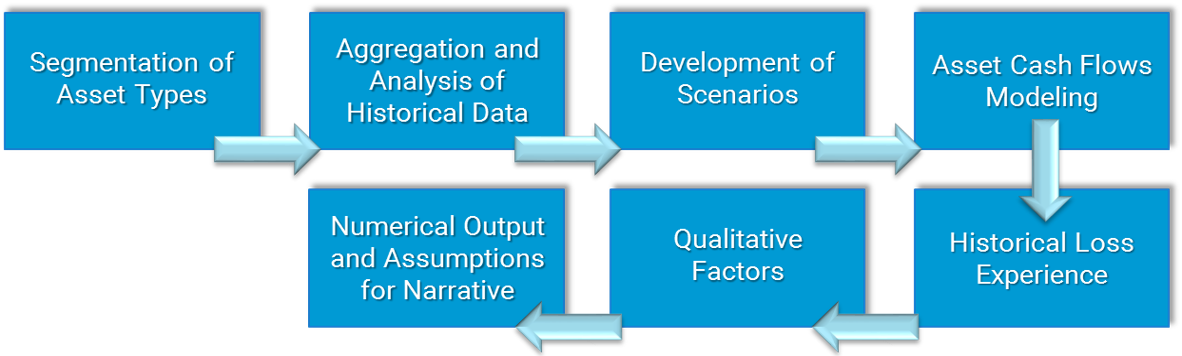

FASB’s CECL Implementation Process

Figure 1: Source: MIAC Analytics

MIAC: Planning for CECL

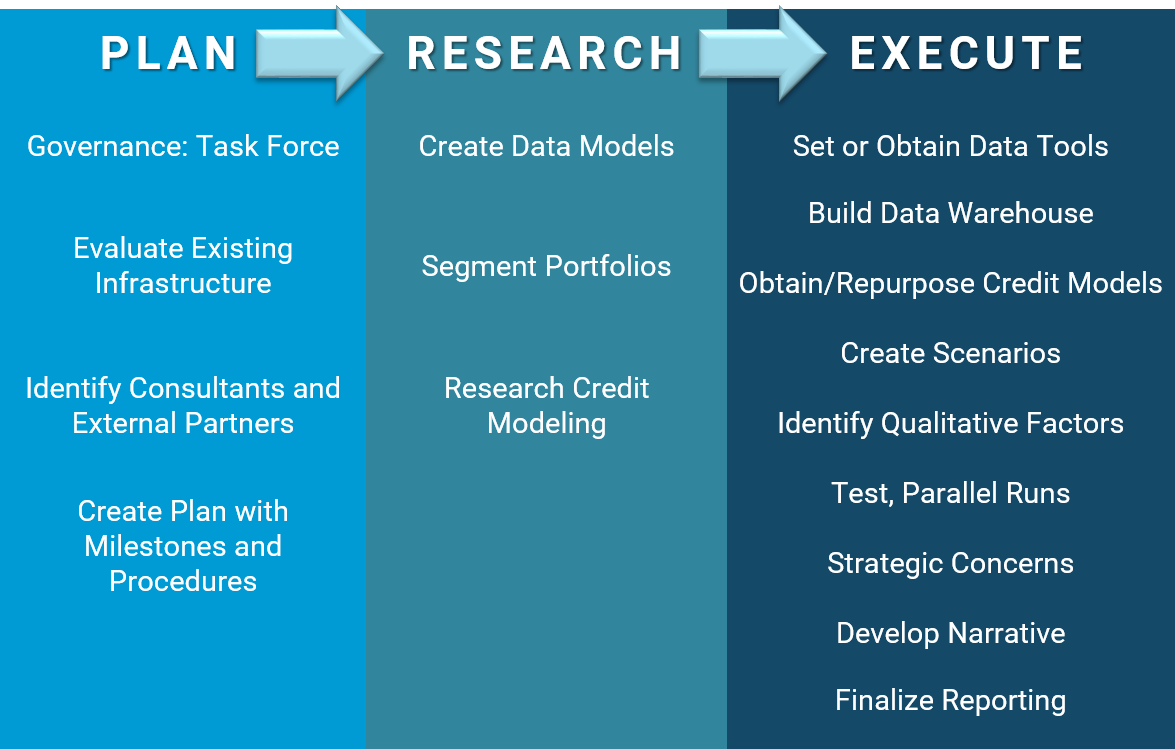

There are definite steps that organizations need to take, and MIAC suggests the following. Start with defining a revised governance standard for CECL, and establish a steering committee or task force with members currently in high-level positions in finance, originations, credit and operations who have management backing. This team needs to be given budget and action authority to implement prescribed procedures.

Then, as required, firms will need to identify appropriate external consultants and partners who can participate and contribute to the process, and should seek ways to integrate them into the process early. These firms should be able to create and/or evaluate models for conformance with the new standards.

Next, these teams will determine the resource needs involved in each area and inventory what exists today, beginning with an initial portfolio segmentation of all loan, lease and debt assets held. Determine what data is needed, what models are needed, as well as technology needs by portfolio.

The committee will need to examine existing models and methods used in the ALLL process to determine which have the potential to meet the new requirements. Generally, cash flow forecasting models offer potential, and static models do not. Firms will perform pilot evaluations of the potential impact of CECL.

These findings will be used to build the “how to” document or “roadmap”. Key objectives and milestones should be along these lines:

-

SEGMENTATION

-

MANAGEMENT

-

METRICS

-

MODELING

-

SCENARIOS

Portfolio Segmentation

Segment the loan, lease and debt portfolio into meaningful segments, so that then, firms can appropriately define data elements needed for each. This leads to the identification of the critical statistical drivers of performance, which will be used in the modeling and reporting, and defining data models.

Data Management

The CECL plan should include the data warehousing and capture infrastructure, tools and data models required, which will require implementation of powerful data capture methods, in monthly snapshots, including credit data and performance data. Firms will need to obtain and reconstruct as much historical data as possible, plus review existing and alternative models, research credit modeling, loss modeling and voluntary prepayment modeling.

Firms must identify models that can be used or repurposed for different products, internal and external, and identify leverage opportunities and efficiency gains from current models, processes, workgroups, modeling approaches (ALLL, DFAST, or internal vs. vendor models).

Develop Metrics and Assumptions

MIAC helps firms use these data models to develop key reporting metrics and descriptions of the drivers used in the credit, loss and prepayment models, determine assumptions, and drive the building of a descriptive narrative of all the models selected and the processes to be used.

Model Design and Development

Institutions will utilize the warehouses and the tools to develop historical analysis and internal models and will integrate results with existing systems. The task will be to expand these systems to handle scenario inputs, and develop financial and managerial reporting formats, as FASB will require lenders to define and explain the use of any credit grading systems and other qualitative inputs to the ALLL process.

Scenario Design

CECL urges banks to develop a narrative to explain the basis of the scenarios and why they are deemed to be reasonable. Regulators will review the scenario rationales with senior management, so institutions are preparing currently with external consultants and auditors.

Firms will begin parallel test runs of the new CECL process and the existing ALLL process. The challenge is to identify: volatility in results and capital impacts, and evaluate strategic considerations across product lines. Naturally, product pricing, origination standards, processing, collections, and operations, will be of the essence.

The CECL Committee is encouraged to work closely with auditors and external partners to finalize the narratives and reporting.

Disclosure Format Examples and Sample Size

FASB provides examples as to what reporting disclosures look like; which are not required formats, but guidance. Internal reports can be tailored to satisfy reporting needs such as allowance aggregation. FASB has also set a requirement (FAS Topic 326) for disaggregation of receivables by credit metric and by vintage year where receivables more than 5 years old are aggregated. The table below is an example.

Figure 2: Source: MIAC Analytics

CECL Partners

MIAC’s core competencies qualify us as a collaborator for CECL planning at financial institutions in the USA and Europe. Our seasoned executive team leads relationships with the most established entities in consumer lending, servicing, and regulation is what sets us apart. Our asset-specific knowledge in whole loan valuation, ALLL, trading and securitization is unrivaled.

The FASB’s prescription essentially mirrors MIAC’s best practices: our methodology and software suite for data warehousing and analytics, due diligence, and borrower behavior modeling is validated and accepted.

Dean Hurley, Managing Director, Structured Products Group

Jeffrey Zuckerman, Vice President, Capital Markets Group

MIAC Perspectives – Summer 2016

CECL – Current Expected Credit Loss: A CORE Competency?

Download MIAC’s FREE CECL Process Guide