Current Expected Credit Loss (“CECL”, ASC 825-15) is the Financial Accounting Standards Board’s (FASB) new model for calculation of loan loss reserves, which requires consideration of multiple scenarios looking out over the lifetime of the instrument. These standards replace those now in use for preparing Allowance for Loan & Lease Losses, (“ALLL”), purchased credit-deteriorated assets, available-for-sale, and held-to-maturity debt securities. [1]

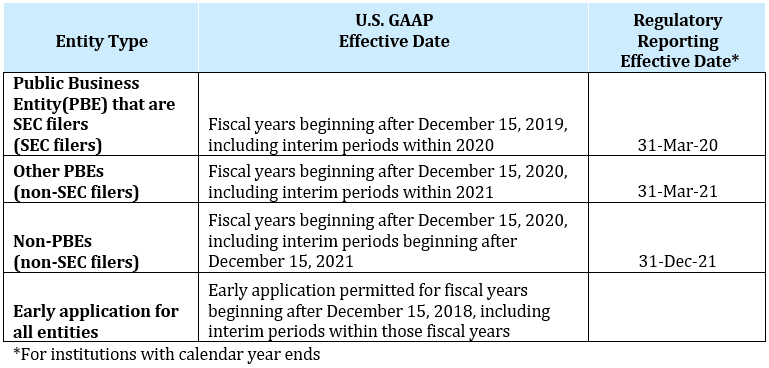

CECL represents a dramatic adjustment for banks, credit unions, and financial institutions, regardless of asset size. Financial institutions will be required to use both historical information and current conditions, in addition to reasonable forecasts to estimate the expected loss over the life of the loan. CECL’s tenets were provided by FASB on June 16th, with joint OCC, FDIC, NCUA and FRB guidance on June 17th. Per the Joint Statement, we expect that more detail will follow, and the standard will be implemented in 2020-21.

This, and other accounting pronouncements introduced since the crisis of the mortgage industry differ from precedent in that the new standards for both reserving and capital adequacy are forward-looking, based upon expectations of future cash flows under plausible scenarios, rather than on historic losses to date.

Comparison of New and Existing Standards

The existing methodology is known as the “incurred loss” approach. CECL is a single measurement approach, which, remarkably, is both a simpler and more sophisticated cash flow and scenario loss modeling approach. The outgoing standards encompass a number of different impairment models. These incurred loss models substantially precluded consideration of possible future losses under possible, but not probable, circumstances. The existing approach has also been known as the Event-Driven Approach.

The new approach is grounded in how mark-to-market cash flows are modeled. Future loss provisioning, or the Allowance for the Loan and Lease Losses, (“ALLL”), may now differ from past experience, and may take into account both individual firms’ loss history and losses that may ensue assuming possible future economic events.

Since the ALLL is a balance sheet reserve for “expected” new losses, the iterative practice is to model the total expected losses for a pool, then subtract the current “charged off” amount to arrive at the current period “provision”. Per the joint supervisory guidance, the ALLL is treated as a valuation account, so revising the definition of what is expected will be powerful, and will drive new requirements for profound enhancements to be made in portfolio data capture, and reporting & risk management procedures.

The ALLL represents “spent money” unavailable for dividends or stock computations.

The revised standard effectively formalizes analytical methods that MIAC has been practicing with our clients for over a decade. Firms will now be required to perform cash flow forecasting for collateral assets segmented into buckets of like characteristics (in contemplation of vintage, geography, LTV, and other factors) blended with lender and servicer experience, and in consideration of macro and micro-economic scenarios.

Why have the changes been implemented?

In the aftermath of the last financial crisis, the outgoing methodology was criticized for not sufficiently incorporating forward-looking information when assessing the need for an allowance for credit losses (the ALLL), for using too broad an approach in forecasting performance on widely differing pools of lenders and loans, and for delaying recognition of changes or problems.

The CECL standard effectively makes sure all future losses under reasonable scenarios are incorporated into the ALLL, which is the gold standard.

Next Steps:

While the regulators are telling financial institutions not to increase their reserves prior to implementing CECL, they are advising that preparation and planning should commence. The stakes are substantial. Thomas Curry of the OCC has said in remarks in September 2013 at the AICPA Banking Conference that it is likely that bank ALLLs could increase by 30% to 50% due to the adoption of CECL. A transition to CECL will require lenders and servicers to adopt detailed record-keeping, track loan-level credit performance in a time series format, validate for compliance purposes, and benchmark their records against industry metrics.

Challenges for many institutions may arise in an arduous process to track performance over time, and to load, audit, reconcile, normalize, and store vast volumes of time series data in a consistent, useful, and accurate manner. There will also be heightened attention on procedures for handling the current period data, including error-checking, data exceptions, and reporting, as these data fields allow accountants and stakeholders to visualize and understand pool composition, forecasting, and provisioning.

While the standards and thresholds are certainly being raised, the new pronouncement allows institutions to apply judgment in developing estimation methods that are appropriate and practical for their circumstances. Lenders will need to establish greater data storage and analytical requirements, and will demand enhanced coordination between functional areas to accurately focus the institution’s talents and judgment for the forecasting of expected losses under the new parameters.

The same standards and practices are generally being applied to smaller institutions as well as larger ones, as the implementation of DFAST, the Dodd-Frank Asset Stress Test, will continue to spell out and specify the levels of capital required, and crucially, what counts as capital going forward.

MIAC Perspective:

MIAC has built advanced analytical tools and provides services to help the lending and accounting profession prepare for this transition and to execute seamlessly.

With specific advances in data management and mining, and comparisons to national populations and including comparison across alternate geographies and vintages, we currently have successfully implemented CECL’s requirements for many institutional clients of various types.

Data Products and Surveillance:

DataRaptor – Surveillance™ is an extension of DataRaptor ® and is used to measure client specific loan portfolio’s collateral payment performance over time. Voluntary prepayments, involuntary prepayments, transition roll rates, FCL_Entry and Exit behaviors and REO_Exit behaviors at the loan portfolio level is measured. Loan portfolios can be auto loans, unsecured consumer loans, credit cards, residential or commercial mortgages, for example. The portfolio specific measurements will feed into models for cash flows valuations based on realized incurred losses, transitional credit events, roll rates, cure rates, timelines and severities observed in portfolios at the loan-level. The granularity and utility of MIAC’s borrower behavior modeling is unmatched.

Due Diligence and Data Scrubbing:

MIAC can help clients fix erroneous and missing data via several means, including due diligence solutions using our VeriFi™ software, or through the use of our historical data analytics to provide appropriate averages or minimums based on the data sets.

MIAC’s unit, Mortgage Delivery Specialists (“MDS”) is recognized as the industry leader in resolving complex data capture and data auditing necessary to enable seasoned residential mortgages successfully delivered to the Agencies.

Behavioral Models:

MIAC has led the way in modeling financial instruments under a variety of macro-economic scenarios, and has tailored models to test for those established by regulators or by institutions. We have produced and maintained proprietary voluntary prepayment, default and loss models which react to macro-economic and loan characteristic scenario variables, as well as customized models for lender and servicer collateral experience.

MIAC CORE™, our loan behavior suite, has proven to be an extremely accurate forecaster of defaults and losses in back testing and out-of-sample tests. This is because our software simulates cash flows with great granularity – at the loan level, period by period, into the future. And, importantly, the simulation starts with the current delinquency status of the loans and evolves forward in the simulation to produce a highly accurate timing of expected losses.

For the Residential Mortgage CORE™ voluntary and involuntary models, we use historical loan level data on approximately 85 million residential loans which span from Fannie, Freddie, Ginnie Mae, and Private Label Securities loan products across the full spectrum of trustees and servicers, going back as far as 1991.

These curves are segmented at the state, servicer and vintage level. Currently, we have unique foreclosure and REO curves on approximately 425 servicers.

MIAC is well-positioned to help our clients adapt to the challenges presented by CECL.

MultiScenario Analysis:

Finally, the client’s inventory of loan assets can be simulated under the same interest rate and macro factor scenarios within the Vision™ balance sheet simulation tool. The multi scenario simulation is important for loans that have embedded options such as residential mortgages. Vision is used for CCAR/DFAST stress testing as well as market risk, capital planning and NII simulations.

[1] Existing Regulatory and GAAP standards include:

- The “Uniform Retail Credit Classification and Account Management Policy”, Federal Register Vol 65, No 113, Monday June 12, 2000

- FAS 5 /ASC 450-20 – General Credit Impairment (Impairment present but not manifested) / Contingencies

- FAS 118 / ASC 450-20 – Troubled Debt Restructuring

- FAS 114 / ASC 310-10 – Non-Performing Loans (Manifested Impairment)

- FAS 141R / ACSC 805 and SOP 03-3 / ASC 310-30– Acquired Loans

- FAS 115 / ASC 325-40 – Interests in securitizations

Dean Hurley, Director, Capital Markets Group

Jeffrey Zuckerman, Vice President, Capital Markets Group

MIAC Perspectives – Summer 2016

CECL – Current Expected Credit Loss: A CORE Competency?

Download MIAC’s FREE CECL Process Guide

Read MIAC’s Case Study: “Bank ABC” CECL Allowance

![]()

CONTACT

CECL@miacanalytics.com